Risk Information

Risk Management System

As the management environment surrounding the Company changes, risks to be managed are becoming more complex and diverse. Under such circumstance, the Company recognizes that one of the most important management issues is to enhance and strengthen the Company's risk management system to fully recognize risks, maintain sound management, and ensure stable profitability and growth. In addition, amid advancement of digital technologies recent years, the Company recognizes risks arising from utilization and delayed introduction of AI and other new technologies as one of the changes in the management environment surrounding the Company and is gradually developing systems to address such risks.

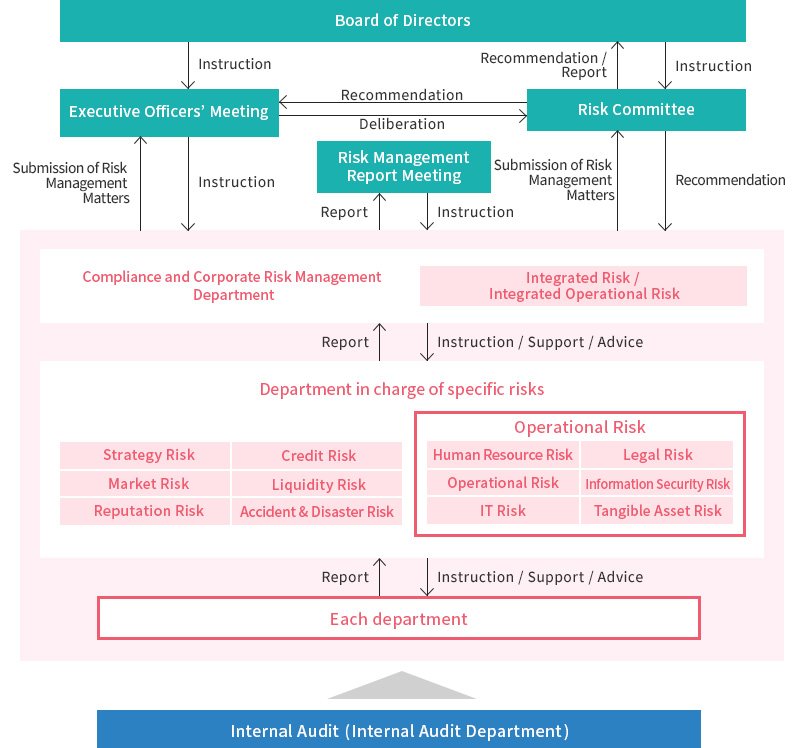

The Company identifies, evaluates, and controls risks regularly through the departments and sections in charge of risks to be managed as stipulated in the Risk Management Regulations, and these risks are managed by the Compliance and Risk Management Department, which consolidates risk management status of the departments and sections in charge, in an integrated manner. With respect to risk management activities in business operations, reports are presented at Risk Management Reporting Meetings. The Risk Committee deliberates on important matters related to risk management, monitors the status of risk management and other activities, and reports the results or makes recommendations to the Board of Directors.

Risk management system

Top Risks

The Company determines the probability of risks based on the probability of risk scenarios and the degree of their impact, and identifies the risk events that require the most attention as top risks. For the identified top risks, the Company assesses increases and signs of such risks and takes necessary countermeasures to prevent and control them. In addition, in the event that a risk materializes, the Company has a system in place to respond promptly.

Top risks are preliminarily reviewed at the Executive Officers' Meeting, discussed by the Risk Committee, and resolved by the Board of Directors each fiscal year.

| Risk events | Risk scenarios |

|---|---|

| Decrease in revenues from business | Decreases in revenues from the loan and credit card business, the guarantee business, and the overseas financial business |

| Increase in credit costs | Increases in provision for bad debts for the loan and credit card business, the guarantee business, and the overseas financial business |

| Materialization of IT risk |

|

| Occurrence of cyberattack damage | Leakage of customer information, and the suspension of service to customers, etc. due to cyberattacks |

| Shortage of human resources | Decreased competitiveness due to shortage of necessary human resources |

| Impact of external factors | Situations in which the Company's business performance is materially affected by external factors such as natural disaster, epidemic, and terrorist attacks |

| Interest repayment | Larger-than-expected amount of interest repayment resulting in an additional provision for loss on interest repayment |

| Materialization of conduct risk | Situations that may significantly affect stakeholders from the viewpoint of consumer protection, maintenance of market integrity, etc. |

| Deterioration of fund procurement | Deteriorated cash flows of the Company due to rising borrowing interest rates, declining operating results of the Company, rating downgrades, etc. |

Of the risks associated with the businesses and others of the Company Group, we have listed major items that could materially affect the decision of investors based on the analysis of the top risks stated above.

This section includes forward-looking statements that are based on assumptions made as of the submission date of this securities report if not stated otherwise.

- Decrease in business revenue

The Company Group has positioned the loan and credit card business, the guarantee business, and the overseas financial business as its three core businesses, and is working on a range of initiatives in a bid to increase revenues from these businesses in a stable and sustainable manner. For the fiscal year ended March 31, 2026, operating revenue came in at 337,709 million yen (up 6.3% year-on-year), of which revenue from the loan and credit card business amounted to 181,889 million yen (up 7.3% year-on-year), revenue from the guarantee business amounted to 81,039 million yen (up 6.2% year-on-year), and revenue from the overseas financial business amounted to 67,526 million yen (up 3.2% year-on-year). These three core businesses represented 97.9% of the consolidated operating revenue.

Risks that could drive down revenues from these businesses are as follows:- 1) Loan and credit card business

- Revenue from the loan and credit card business fluctuates depending on increases/decreases in the number of customer accounts, increases/decreases in the loan balance per customer account, the average contracted interest rates received from customers, and other factors. Therefore, external factors related to these elements could affect the segment's business performance.

In addition, a decrease in competitiveness with rival companies due to a lack of ability to provide IT services that suit to customers' needs could also affect the segment's business performance.

Such external factors include changes in judicial rulings and legal regulations applicable to the consumer finance industry, intensified competition with rival companies, entry of new companies, a slowdown in consumer spending in the wake of large-scale accidents, disasters and the spread of epidemics.

The loan and credit card business represented 53.9% of total operating revenue, and in light of the fact that a decrease in revenues from this business segment would have a significant impact, the Company is striving to attract new customers, improve product/service functions and take other initiatives.

In addition, the Group has systems to regularly manage and analyze changes in interest on operating loans from the plan and report these changes and various countermeasures to the Risk Management Report Meeting and the Risk Committee, and appropriately controls risks.

- 2) Guarantee business

- Revenue from the guarantee business fluctuates depending on increases/decreases in the number of guarantee accounts, increases/decreases in the balance per account, guarantee commission rates from partnering financial institutions, and other factors. Therefore, external factors related to these matters could affect the business performance of the Company and MU Credit Guarantee Co., LTD.

Such external factors include changes in judicial rulings and legal regulations applicable to financial institutions such as banks and a slowdown in consumer spending in the wake of large-scale accidents, disasters and the spread of epidemics.

The guarantee business represented 24.0% of total operating revenue, and in light of the fact that a decrease in revenue from this business segment would have a significant impact, the Company and MU Credit Guarantee Co., LTD. worked on measures to enhance partnerships with existing partners, continued appropriate screening, provided the results of analysis about loan portfolio and the effect of advertisement, and offered various support to existing partners with a view to enhancing their business results and stabilizing their growth.

In addition, the Group has systems to regularly manage and analyze changes in revenue from credit guarantee from the plan and report these changes and various countermeasures to the Risk Management Report Meeting and the Risk Committee, and appropriately controls risks.

- 3) Overseas financial business

- Revenue from the overseas financial business fluctuates depending on increases/decreases in the number of customer accounts, increases/decreases in the loan balance per customer account, the contracted interest rates received from customers and other factors. Therefore, external factors related to these matters could affect the business performance of EASY BUY Public Company Limited (hereinafter "EASY BUY") in the Kingdom of Thailand and ACOM CONSUMER FINANCE CORPORATION (hereinafter "ACF") in the Republic of the Philippines, in addition to ACOM (M) SDN. BHD. (hereinafter "ACM") in Malaysia.

Such external factors include changes in the impact of interstate conflicts and resulting economic sanctions, judicial rulings and legal regulations applicable in countries where these companies operate, intensified competition with rival companies, a slowdown in consumer spending in the wake of large-scale accidents, disasters and the spread of epidemics, as well as fluctuations in foreign exchange rates.

The overseas financial business represented 20.0% of total operating revenue, and in light of the fact that a decrease in revenue from this business segment would have a significant impact, the Company is striving to attract new customers, improve product/service functions and taking other initiatives at three subsidiaries: EASY BUY, ACF and ACM.

In addition, the Group has systems to regularly manage and analyze changes in operating revenue of EASY BUY, the largest consolidated subsidiary in the overseas finance business, from the plan, and report these changes and various countermeasures to the Risk Management Report Meeting and the Risk Committee, and appropriately controls risks.

- Increase in credit costs

For accounts receivable - operating loans, accounts receivable - installment and right to reimbursement, which constitute the majority of total assets of the Company Group, we have recognized provision for bad debts (the sum of provision of allowance for doubtful accounts and provision for loss on guarantees, etc.) and estimated values of collaterals pledged, etc. However, an increase of payment delays might occur as a result of decline in customers' creditworthiness due to potential future changes in economic conditions, the market environment, and the social structure in Japan as well as revisions in legislation. Such events could require further increases in provision for bad debts, and as a result, may have a negative effect on the business performance of the Company Group.

Therefore, the Group will regularly monitor customers' creditworthiness to maintain the soundness of the loan portfolio. - Materialization of IT risk

The Company Group has a large-scale computer system and processes personal data and other information using a communication network and systems at each of our business locations, as well as those of our customers and other external parties connected to our group, and strives to appropriately manage and handle information.

However, the Group may not be able to completely prevent system outages, malfunctions or unauthorized use of systems, falsification or leakage of electronic data, or the suspension of support services by telecommunications carriers and computer system companies in the event of delay in the planning and development of critical IT system projects, system failures, cyber-attacks, unauthorized access, computer virus infections, disasters, or other exogenous events.

In such cases, the provision of customer services and our group's business operations may be hindered, trust in our group may be damaged, and our business performance may be affected.

To ensure the stable operation of its systems, the Company Group has made efforts to prevent system failures and other problems by monitoring throughout system planning, development, and operation, and has put in place management structure and procedures to reallocate resources and prepare for unforeseen events, as well as training and other measures. - Occurrence of cyberattack damage

In recent years, amid the advancement of AI and other digital technologies and rising geopolitical risks, cyberattacks have been becoming increasingly sophisticated and complex on a daily basis. Cyberattack-related risks include not only system shutdowns, but also the potential leakage of customer information and other sensitive data.

If cyberattack damages are materialized, the provision of customer services and the Company Group's business operations may be hindered, trust in the Company Group may be impaired, and our business performance may be adversely affected.

The Company Group has established a cyberattack response system that functions in both normal and emergency situations in order to prevent the occurrence of damage caused by cyberattacks. As specific security measures, we are promoting the development of procedures and manuals related to cyberattacks, the collection of vulnerability information and implementation of corresponding countermeasures, as well as regular training and drills. - Shortage of human resources

If the necessary human resources cannot be adequately secured due to the external environment, such as the shrinking workforce and the mobilization of human resources, it could have an impact on the Company Group's sustainable growth.

Promoting diversity based on the corporate philosophy, we respect the abilities, ideas and values of our diverse human resources and engage in making a working environment where employees can feel job satisfaction and comfort.

We strive to improve job satisfaction and workplace comfort through various initiatives, including increases in base salary and bonuses, introduction of an IT skill certification system, improvements to personnel systems and employee benefits such as allowances and leaves, initiatives to ingrain the Vision, and support for self-development.

In addition, while securing human resources by recruiting excellent and promising new graduates and mid-career employees, we are striving to enhance the training system, including selective training and digital human resource development program, based on the Policy on Human Resource Development. Furthermore, we are actively working for human resource development aiming at improving employees' literacy, by, for example, supporting acquisition of AI-related qualifications. - Situations in which the Company's business performance is materially affected by external factors, accidents, and disasters, etc.

Natural disasters, such as large-scale earthquakes, volcanic eruptions, wind and flood damage, spread of infectious diseases, conflicts, and terrorist attacks in the highest concentrated areas of our business bases such as the Tokyo metropolitan area could cause damage to our facilities and equipment or physical damage to employees or customers, and as a result, could have a negative effect on the performance and business continuity of the Company Group.

To prepare for unforeseen events such as these, the Group has formulated a business continuity plan and prepared a backup system that includes call centers and core systems.

In addition, the Group strives to develop and strengthen systems to ensure the continuity of critical business operations by defining the reporting lines and roles and responsibilities at the time of emergency, ensuring an appropriate stockpile of emergency supplies and regularly conducting education and training to improve the effectiveness of such responses. - Interest repayment

The interest rates charged on some loan products by the Company, in which customers entered into contracts before June 17, 2007, exceed the interest rate ceilings specified in the Interest Rate Restriction Act.

In case our customers request a reduction in the loan amount or reimbursement of excess interest paid for such cases citing past judicial rulings, the Company may accept to write off such loan or reimburse payments. Though the costs of write-off and reimbursing repayments (hereinafter referred to as "loss on interest repayment") have steadily decreased, close attention should be paid to the number of requests for interest repayment. Future potential for loss on interest repayment, further booking of the provision for loss on interest repayment, and court rulings from lawsuits demanding refunds of interest paid that put the Company and other money lenders at a clear disadvantage, could have an impact on the Company's business performance.

Considering that loss on interest repayment has been consistently decreasing each fiscal year since the fiscal year ended March 31, 2011, the peak period, it is thought that the possibility of a sharp increase in interest repayment is limited. However, future trends need to be closely monitored on an ongoing basis, as loss on interest repayment is susceptible to the impacts of changes in the external environment.

In addition, with respect to loss on interest repayment, we reassess the provision for loss on interest repayment at the end of each fiscal year by forecasting future trends based on historical data. If the provision is deemed insufficient, additional provisions are recorded. Furthermore, we conduct appropriate risk control by monitoring on a quarterly basis whether there have been any significant changes from the future trends forecasted at the time of the most recent reassessment. - Materialization of conduct risk

Any inappropriate behavior or deviation from social norms by an officer or employee, or any inappropriate business operation could result in an impairment of trust in the Company Group and adversely affect the Company Group's business performance and corporate value through loss of customers, decrease in trade opportunities, materialization of risk of administrative penalty. etc.

The Company Group has established the ACOM Group Code of Ethics and Code of Conduct, which set forth the basic values and policies for practicing compliance. Through training programs for officers and employees, the Company has been striving to foster a compliance culture to implement correct behavior.

In addition to development and enhancement of internal control system to prevent violations of laws and regulations and misconduct, the Company Group promoting various measures to protect customers, such as consumer education activities, stricter credit operations, and financial crime countermeasures. - Deterioration of fund procurement

The Company Group secures the necessary funds for its operations and liabilities repayments through borrowings from financial institutions, etc. and financing from capital markets, including via bond and commercial paper issues.

On the other hand, there is a possibility that its existing main banks and lenders will change their current lending policy due to a potential reorganization of the financial industry or other factors. Furthermore, there is no assurance that capital markets will always be available as a reliable financing resource in the future.

In addition, if the funding environment were to deteriorate due to a sharp rise in market interest rates, a decline in the Company's business performance, or a downgrade in its credit rating, there is a risk that the necessary funds may not be secured or that funding may have to be obtained at significantly higher interest rates than usual, which could adversely affect the business performance of the Company Group.

Accordingly, in order to ensure appropriate and sound business operations, the Company Group promotes the diversification of funding sources, such as corporate bonds and commercial papers, and maintains an adequate level of cash on hand. In addition, the Company Group works to mitigate liquidity risk by establishing liquidity backup facilities such as commitment lines. Furthermore, the Company Group manages interest rate fluctuation risk appropriately by maintaining a certain proportion of fixed-rate funding and adjusting the balance between short- and long-term funding in accordance with market conditions.

In order to smoothly raise funds from capital markets, as of March 31, 2026, the Company has acquired ratings of AA- for long-term debt from Rating and Investment Information, INC. (R&I), AA- for long-term debt and J-1+ for commercial papers from Japan Credit Rating Agency, Ltd. (JCR).

Business Continuity Plan (BCP)

The Acom Group has formulated BCP to ensure the safety of employees and their families in the event of natural disasters such as large-scale earthquakes, the spread of infectious diseases, terrorist attacks and other crisis events, while ensuring that significant business operations are not interrupted or, if interrupted, that they are resumed as swiftly as possible.

As specific activities, we have established two business locations, prepared a crisis management manual and stockpiled food and drinking water to minimize economic losses and loss of credibility.

In addition, we conduct evacuation drills and safety confirmation drills, and once a year we conduct a joint business continuity drill with the MUFG Group to promote cooperation among the Group companies.